The new survey by JLL and ACW captures a sector that is no longer growing at random and has begun to choose: it is professionalising, polarising, concentrating. The report’s figures tell more than one story.

Coworking is dismantling, piece by piece, the premises from which it was born. And it is doing so precisely as its own accounts prove that those premises were its principal asset.

The Radiografía del Sector de Coworking y Oficinas Flexibles en España by JLL and ACW (first quarter 2026) is a full photograph of the sector: 181 centres, roughly 304,000 square metres under management, 20 cities. It records what the market does, not what operators say they do.

The official thesis is reassuring: the sector is maturing, professionalising, consolidating. My reading, through the same figures, is less comfortable than the one, correct as far as it goes, that the report tells. Coworking is slowly forgetting why it was born.

Professionalisation Is Also a Liquidation

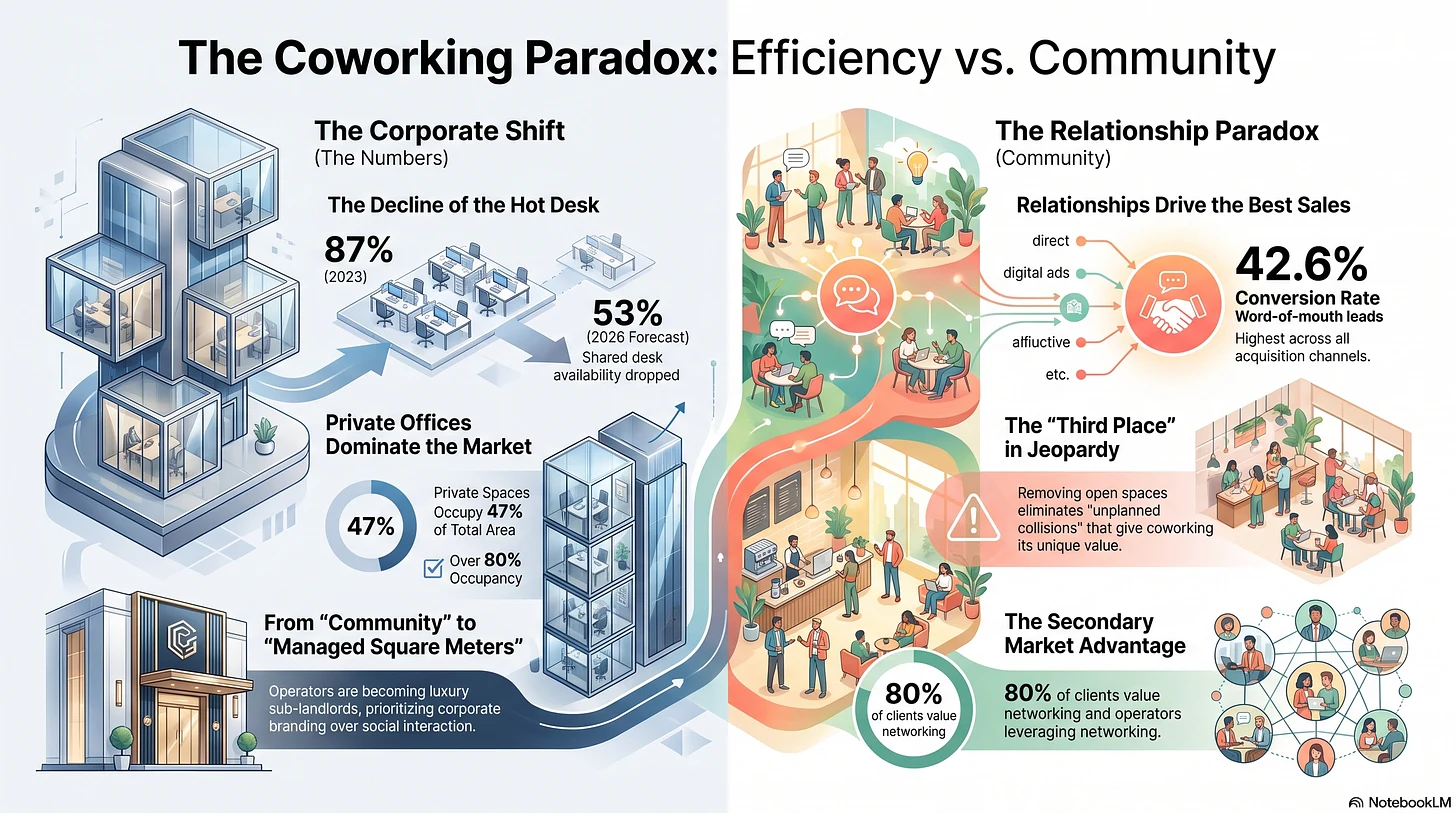

The sharpest figure in the report marks the end of an era.

The hot desk, the open shared desk, the very symbol of coworking in its early days, was offered by 87% of operators in 2023. In three years, a third of the sector has scrapped the service, and we are down to 53%.

Private offices now account for at least 47% of the sector’s floor space, and more than seven operators in ten run them above 80% occupancy. It is, by some distance, the product that holds up best.

In between, a third model is growing, the managed office: bespoke space, carrying the client company’s identity, but without the commitments of a traditional lease. Privacy, brand, control. The report presents it as good news for the books, and in large part it is. But what does it amount to, in practice?

In a managed office, the operator takes on the space, fits it out, and lets it under the client’s name, keeping on its own shoulders the property risk the company no longer wants on its balance sheet. It is a valuable service. It is also, looked at closely, a different trade.

The operator stops selling community and services and starts selling fitted square metres with a margin on top. It becomes a luxury sub-letter: a real-estate and financial business, no longer a business of relationships.

The distance from the traditional office, once again, narrows.

The report reads all this as a sign of maturity, and it is true. But it is half the truth. Because what we call professionalisation is also the dismantling of what sets coworking apart from any other office. The open space was uncomfortable, noisy, and poorly profitable per square metre. It was also the one thing coworking had, and the corporate office did not. The sector is winning the efficiency race by becoming exactly what it claimed to be the alternative to: the corporate office, with a better coffee and even a nice sunset terrace, plants and all.

What Shrinks Is Not the Desks

It would be easy to stop at nostalgia for shared desks, and it would be wrong. No one misses the noise or the lack of privacy. The demand for private offices is real and legitimate, and operators are right to meet it: people come to work to concentrate, not to socialise on command.

Removing the open space does not mean merely losing one kind of workstation. It means removing the mechanism that sparks the relationship.

The value of coworking was never the desk: it was the collision, the unplanned encounter between people who were not looking for one another and who, for exactly that reason, find one another.

It is the principle of the “third places” described by Ray Oldenburg forty years ago: spaces that are neither home nor work, where community forms through friction, not by appointment. Remove the friction, and what remains is a block of closed doors.

Coworking that shuts itself into private rooms solves a problem of concentration and creates one of meaning. It becomes more efficient and less necessary.

More orderly, more replaceable.

I have written about these third places recently from the other side: coworking as the unwitting heir to a civic infrastructure that society has stopped producing. There, I looked at it from outside, from the position of those who have lost their places of community. Here, I look at it from within, from the position of those who run those places, and risk dismantling them with their own hands.

The Numbers That Clear Things Up

The report demonstrates, with a single figure, the exact opposite of what the sector is doing.

The most used acquisition channels are the direct ones, around 62% of volume. But if you look at conversion, that is, how many deals actually close, the ranking flips. Clients who arrive by word of mouth convert better than any other: 42.6% on average, up to nearly 50% among the large operators. Networking, relationships, and the recommendation of someone who had a good experience: this is the most profitable commercial channel in the whole sector. Not an extra, not a soft value for the brochure. The hardest economic lever the report measures.

Put the two facts together. On one side, the sector dismantles community as a product: out go the open desks, out goes the collision, in behind the doors. On the other hand, it lives on community as an engine, because it is relationships that keep clients.

Coworking sells privacy and lives on word of mouth.

It is sawing off the branch on which the fruit it feeds on ripens.

There is another clue in the same direction. Meeting rooms, once a competitive advantage, are now held by 98% of operators: they have become a standard, not a difference. The new frontier, JLL says, is event space. An event is an organised collision: the way a physical space produces what a screen cannot replicate. Even as it closes the desks, the sector is trying to reassemble the community under another name.

Málaga, or the Truth as Seen from the Inside

I should say where I operate, because it changes the weight of what I write. I run two coworking spaces in Málaga, and this report’s taxonomy places me, without mercy, in the uncomfortable spot.

The report classifies operators by size and by location: inside or outside Madrid and Barcelona. Those outside the two big cities, and so Innovation Campus too, land in the tiers the survey describes in its harshest terms: secondary markets, trapped in a price war, exposed to a structural vulnerability the prime operators do not know. The large players, in prime locations, can afford premium rates, aggressive expansion, and clients who pay for customisation over price. The secondary cannot. The secondary, the report says, competes at the bottom or does not compete.

It would be convenient to pretend not to be there, to tell Málaga as the exception: the city that draws multinationals and high-earning nomads, named in the report right after Madrid and Barcelona. It is true, and it is good news for the city. But it does not change the geometry. The operator working here stays on the sector’s map, in the exposed square. Holding the two things together, the pride of being in a city on the rise and the clarity of occupying a fragile position, is more honest than telling only one of them.

And here the uncomfortable position becomes, looked at properly, the strategic clue.

The Bet of Those Who Cannot Win the Wrong Race

Those in the secondary market will never win the war of scale and privacy.

They do not have the square metres, the rates, or the locational rent of the prime zones. Chasing the big players on their own ground (more closed offices, more premium, more efficiency per square metre) is a race lost from the start: it is their race.

One lever remains, and it is precisely the one the figures reward and the sector undervalues: relationship. Word of mouth that converts. The events that fill a space when the screen threatens to empty it. Community turned back into infrastructure: a value the report measures in conversion points, not in square metres.

This is not a hope of mine; it is once again in the data, and it touches me closely. The two spaces we run in Málaga, of roughly 1,600 and 750 square metres outside the big cities, both fall into the same tier: mid-sized operators, far from Madrid and Barcelona. And it is exactly the tier the report records as the most community-oriented: over 80% offer networking, and half their clients say they value it. The secondary market of my size does not need to invent its own lever. It already has it. The risk is that it forgets it while chasing a model that does not belong to it, just as the radiografía shows that this lever is the most profitable in the trade.

There is a final irony, and it is the most serious. The push towards privacy, scale, and the closed office is rational at the level of the single operator: each choice makes positive sense on the balance sheet. But added together, those choices risk liquidating the one thing that gives coworking a reason to exist, distinct from the corporate office. It is one way a sector can optimise itself into irrelevance: one sensible decision at a time.

The report says the sector will grow by almost 16% on average in 2026. But the average matters little: what will matter is who has understood what is changing, not only how much. The private offices that win, the events that go back to making the difference, a secondary city discovering itself as a centre.

If I were a betting man, I would say 2026 will reward those who have understood that their asset was never the desk, but what happened when two people, in front of a desk, spoke to one another without having made an appointment.

Yet here a fault line opens, and it is not a matter of poetry but of accounts. If a relationship is the lever that converts best, then

the community has a precise economic value. And today, the market does not know how to price it.

We know what a square metre of private office is worth, what to charge for fibre or air conditioning; we have no price list for the density of relationships. As long as management software counts only the closed rooms and ignores word of mouth, we will go on optimising the square metres and impoverishing the business.

But putting a price on community is another reckoning and another balance sheet. Perhaps one for a future article.